Regulatory procedures in India can often be slow and long-drawn, but banks appear to have wasted no time in implementing the RBI’s recent guidelines on cryptocurrencies.

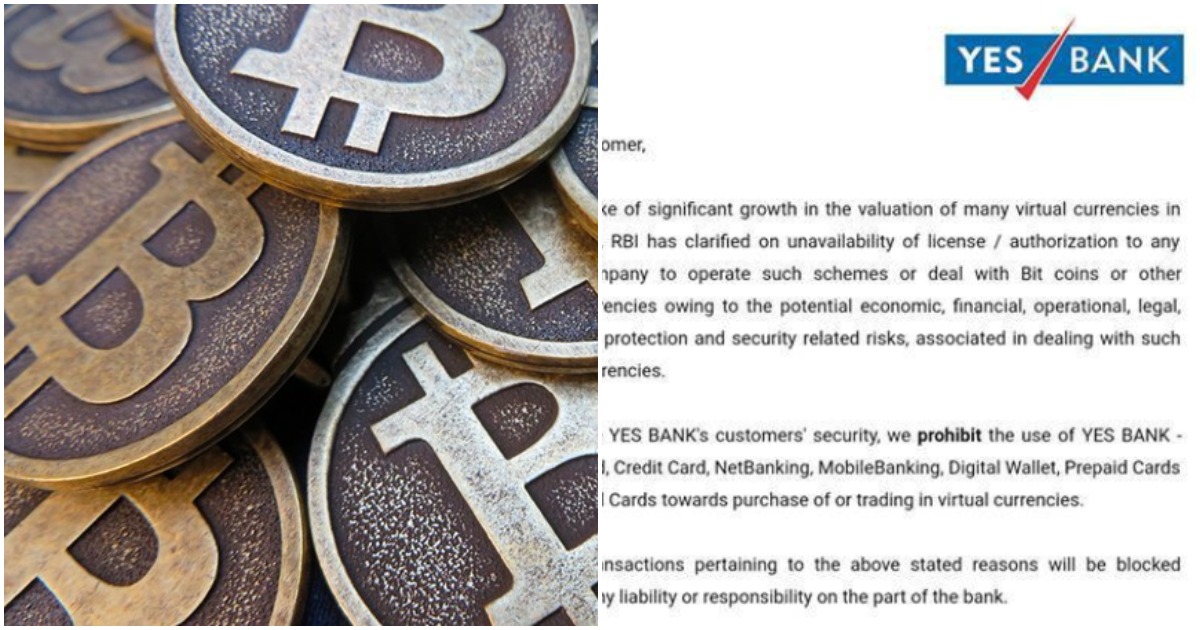

Yes Bank has already sent its customers emails saying that their services can be no longer be used to purchase virtual currencies. “To ensure YES Bank customers’ security, we prohibit the use of YES BANK — Debit Card, Credit Card, NetBanking, Mobile Banking, Digital Wallet, Prepaid Cards and Travel Cards towards purchase and trading in cryptocurrencies,” said an email received by some customers. “Future transactions pertaining to the above stated reasons will be blocked without any liability or responsibility on the part of the bank,” the email added.

Dear @YESBANK,

F**K YOU#RBICantStopMe : Seems like they can!! ?Raise your voice against @RBI's Worst decision ever by signing this petition below ??https://t.co/wdNBmUhzQn#Bitcoin #Litecoin #cryptocurrency #crypto #ethereum #zebpay #cryptoban #isupportcrypto pic.twitter.com/7pk9UQTSLa

— Crypto India News (@CryptoIndiaNews) April 6, 2018

ICICI Bank has sent its customers a similar mail. ‘To ensure the security of our customers, the bank will not allow usage of ICICI Bank Credit, Debit, and Prepaid cards…towards purchase and trading of such bitcoins, cryptocurrencies or virtual currencies at merchants suspected to be dealing in cryptocurrencies,” the bank said.

look here @ICICIBank also have discontinue. pic.twitter.com/cMZjBJfj3n

— satyen (@satyen2017) April 9, 2018

We’re still trying to determine if other banks have sent similar missives, but orders of this nature will all but kill India’s burgeoning cryptocurrency markets. India’s crypto traders and investors typically use their bank accounts to transfer money to India-based crypto exchanges such as Zebpay and Unocoin, who in turn exchange their Indian Rupees for the cryptocurrencies of their choice. By prohibiting people from using their Indian Rupees in their bank accounts, Indian users will no longer be able to buy cryptocurrencies.

That’s exactly what the Reserve Bank had mandated when it had banned the authorities it regulates, which includes banks, from dealing with cryptocurrency exchanges. ““In view of the associated risks, it has been decided that, with immediate effect, entities regulated by the RBI shall not deal with or provide services to any individual or business entities dealing with or settling VCs (virtual currencies). Regulated entities that already provide these services shall exit the relationship within a specified time,” the RBI had said on 5th April.

The move had sent shockwaves through India’s crypto currency world. Even as most crypto exchanges had refrained from initially commenting on the issue, investors had taken to Twitter and Facebook to wonder what would become of their cryptocurrency investments. The RBI’s move doesn’t come into place until three months from now, but crypto prices in India had fallen below global levels as investors had scrambled to sell some of their holdings in face of the uncertainty.

Indian prices of cryptocurrencies have since stablilized, and the crypto community, for its part, its trying to drum up support for its cause through change.org petitions. It’s unclear if that’ll have much impact on how the RBI sees the sector as a whole, but some crypto exchanges have been giving indications that they’re looking for ways to circumvent the RBI ban. Crypto exchanges in India now effectively have three months to find a way to find a way around government regulations, but initial signs, including the YES Bank and ICICI Bank orders, seem to show that a rocky road awaits India’s crypto community.