Mutual funds are everywhere these days – celebrities on TV earnestly tell you they’re ‘sahi hai’, investment advisors can’t seem to get enough of them, and slick new-age apps help you start putting your money in them. The mutual funds industry has boomed in recent years – mutual fund assets under management have grown from Rs. 7.31 trillion in 2011 to Rs. 33.06 trillion in 2021, registering a five-fold increase. In the last six years alone, the number of investors in mutual funds has doubled, growing from 4.98 crore in 2015 to 9.78 crore in 2021.

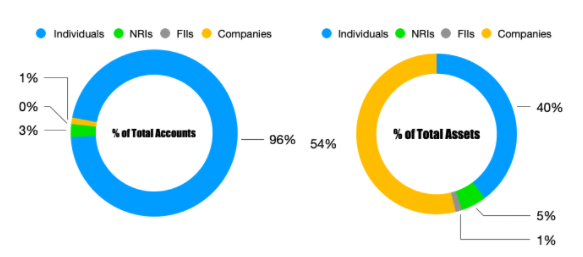

But mutual funds primarily remain an investment vehicle for individuals – millions of companies across India prefer keeping their cash in the safety of their current accounts. Current account balances are safe and can be withdrawn immediately, but they have a downside – they earn no interest. A company with a sizable amount in its current account can, theoretically, put a portion in mutual funds, and likely earn a higher rate of interest. But there are several reasons why they don’t.

Why most companies don’t invest in mutual funds

1. Regulatory requirements: There are several regulatory requirements that companies must first fulfill before they invest in mutual funds. The board must pass a resolution that allows the companies to invest in mutual funds, and should also set limits, if any. The company also needs to fill a non-individual KYC form that requires the balance sheet of the last two years. The company then needs to submit its application to the Asset Management Company with a copy of memorandum and articles of association, certificate of incorporation, and other documents. If the application is in order, mutual funds units are transferred to the company.

2. Liquidity: Withdrawals from most mutual fund schemes can take a while – if a company urgently needs cash, it might be a long and cumbersome process to sell the mutual fund, and then finally get the cash in your bank account.

3. Risk: Mutual funds are diversified investments, but they don’t quite carry the certainty of a current account. Mutual fund values fluctuate on a daily basis with the movements of the stock market, and there’s a real risk that the invested sum might actually decrease by the time you need to withdraw.

4. Taxation: Mutual funds gains are taxable, and that requires even more compliance from companies.

Can companies invest in mutual funds?

It’s not easy for companies to invest in mutual funds, but given the chasm in interest rates – current accounts earn 0% interest, while mutual funds can return as much as 15 percent a year – there might be a case to be made for more companies to begin putting a portion of their working capital in mutual funds. Here are some ways companies can get around to investing in mutual funds.

1. Liquid mutual funds: There are several mutual funds which are quite liquid – these mutual fund units can be converted back into cash within 24 hours. Such mutual funds can be a viable option for companies who might need access to their money at short notice.

2. Debt funds: Equity-based mutual funds can be volatile, and it’s possible that they give mediocre or even negative returns over the short term. Debt funds, though, are less volatile, and can give more predictable returns to companies.

There does appear to be potential for companies to allocate a portion of their working capital towards mutual funds. Putting some money into the right mutual funds could possibly help some companies better organize their finances, and earn returns on spare cash which might’ve otherwise been lying dormant in their current accounts.